「ベトナム国内でもっと展開したい!売上を増やしたい!」

その際、拡大のために支店を持とうかな?という選択を検討している社長様もいると思います。

こんにちは、マナボックスの菅野(すげの)です。

ベトナムで支店を設立する際、企業は、「独立支店」とするか「従属支店」とするかを任意に選択することができます。

※この点、この記事では、「独立支店」を独立に会計帳簿を持つケースとします。そして、「従属支店」は本社と一体となる場合として定義します。

本日は、支店の「独立支店」とするか「従属支店」と税務申告(VAT及びCIT及び事業税)について説明して行きたいと思います。

これを読んで頂ければ、ベトナムの支店と税務について整理できるはずです。

以下の視点で解説していきますね。

- VAT(付加価値)はどうするのか?

- 事業登録税(Business licnese)の取り扱い

- CIT(法人税)の取り扱いは?

この記事のもくじ

VAT(付加価値税)はどうするのか?

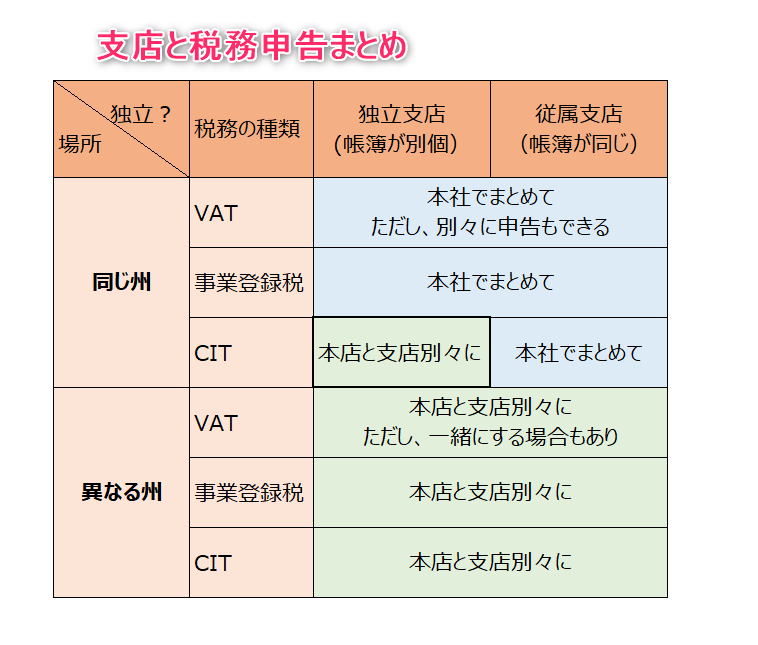

結論は以下の通りです。

- 支店が同じ省→まとめて

- 支店が違う省→原則別々に。例外まとめて。

この点、詳細は、Circular No. 156/2013/TT-BTCの第11条1項b c号に記載されています。

b) Where the taxpayer has an affiliate in the same province or central-affiliated city (hereinafter referred to as province) as the taxpayer’s headquarter, the taxpayer shall file a joint VAT declaration.

If the affiliate has a seal, deposit account, directly sells goods or services, declares sufficient input and output VAT, and wishes to declare tax separately, it must apply for permission to declare tax separately and use separate invoices.

Directors of local Departments of Taxation shall decide the place where providers of restaurant, hotel, massage, and karaoke services declare their tax.

c) Where the taxpayer has an affiliate in another province than the taxpayer’s headquarter, the affiliate shall directly submit the VAT declaration to the supervisory tax authority. If the affiliate does not sell anything and thus does not earn any revenue, tax shall be declared at the taxpayer’s headquarter.

Where the taxpayer plans to sell real estate in another province than that of the taxpayer’s headquarter and establishes an affiliate (branch, management board, etc.), then the taxpayer must apply for tax registration and use credit-invoice method to pay the tax on real estate trading to the tax authority of the locality where real estate is sold.

支店が同じ省の場合はまとめて

すなわち、支店が同じ場所にある場合にはVATはまとめて申告します。

しかし、ある条件を満たせば(会社印をもっている。銀行口座が別々にある。商品を直接販売している。など)、税務署の許可を得て別々で申告することができます。

そのため、独立支店の場合には、省が同じであっても別々に申告することが多くなりそうです。

支店が他の省の場合は、別々に

一方で、支店が他の省にある場合は、VAT申告は別々にしなければいけません。例えば、ハノイに本社があって、ホーチミンに支店あるケースですね。

この場合でも、仮に、当該支店が販売活動をしておらず、収益を計上していない場合、本社と合わせてVATを申告します。

事業登録税の場合は?

事業登録税については以下をご参照ください。

結論は以下の通りです。

- 支店が同じ省→まとめて。

- 支店が違う省→別々に。

以下のように規定されています。

Article 17. License tax

- Tax declarations shall be submitted to supervisory tax authorities.

If the taxpayer has an affiliate (branch, store, etc.) in the same province, the tax declarations of the affiliate may be submitted to the taxpayer’s supervisory tax authority.

If the taxpayer has an affiliate (branch, store, etc.) in another province, the tax declarations of the affiliate may be submitted to the supervisory tax authority of the affiliate.

If the taxpayer does not have a permanent business location, tax declarations shall be submitted to the supervisory Sub-department of taxation of the business or where the taxpayer resides.

基本的にはVATと同じのようです。

CIT、法人税の場合は?

結論は以下の通りです。

- 独立支店の場合→支店ごと

- 従属支店の場合→まとめて

この点、詳細は、Circular No. 156/2013/TT-BTCの第12条1項b c号に記載されています。

Article 12. Declaring corporate income tax (CIT)

Responsibility to submit CIT declarations:

b) Where the taxpayer has an affiliate that keep accounting records independently, the affiliate shall submit its tax declarations to the supervisory tax authority.

c) Where the taxpayer has an affiliate that does not keep accounting records independently, such affiliate is not required to submit tax declarations. The taxpayer must include the tax incurred by the affiliate in the CIT declaration.

基本的には場所という視点ではなく、「独立」か「従属」と言う点で取り扱いが異なってきます。

すなわち、会計帳簿を独立して作成しているかしてかそうでないかです。

●「独立支店」の場合

独立支店は、支店で帳簿を管理しているので、当該支店の財務諸表に基づいてCITを申告・納税します。つまり、別々に申告します。

●「従属支店」の場合

従属支店は、本店に全ての会計に関する証憑書類を送付し、本店は、従属支店の財務諸表も合わせて企業全体の所得を計算してCIT(法人税)を申告・納税します。

ベトナムの支店におけるその他論点

以下について簡単に説明します。3200/TCT-KKというオフィシャルレターを参照しました。

- 税管轄と税番号

- インボイスの発行

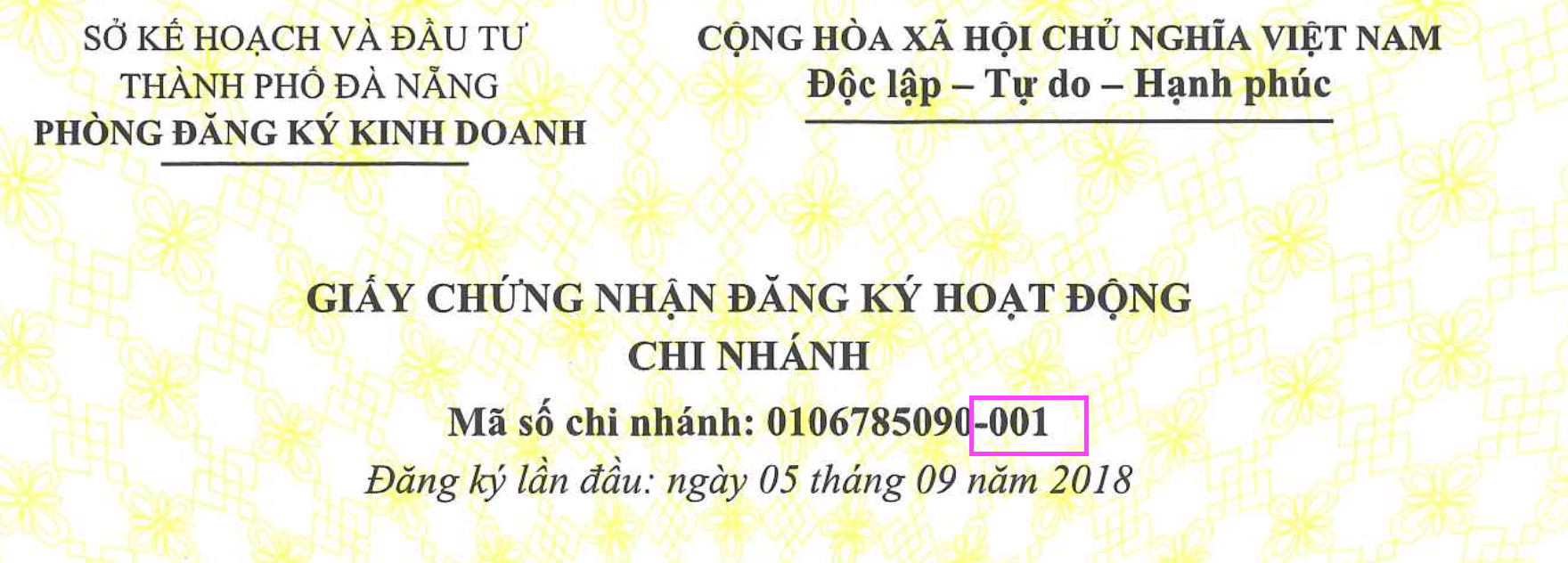

まず、税管轄と税番号です。これは異なる省であればそれぞれの管轄となります。たとえば、ハノイに本店があり、ダナンに支店があれば、それぞれの税務署(ハノイかダナン)の管轄となります。

また、支店の税番号(MST)は、本店の10桁の番号に3桁の番号を追加します。合計13桁の税番号になります。

イメージは以下の通り。

インボイスも、省ごとに発行することになるので、もし、支店で売上を計上する場合には、その支店がある省の税務署に通知を発行する必要があります。ただ、そうではなく本店の売上であれば、特段この手続は必要ありません。

★本日のまとめ★

シンプルにまとめると、、、、。

①支店の場所で判断する。(Province、省ですね。)

②独立的か従属的かで判断する。(帳簿が独立的かどうか?)

という風に整理できます。

あなたの会社が、ベトナムの支店を理解することにより、正しい判断ができることを祈っていますね。

ベトナム会計でお悩みはありませんか?

マナボックスにはベトナム歴9年の日本公認会計士と実務経験豊富なベトナム人会計士が、VATの実務上の留意点についても相談させて頂きます。

問い合わせページより、気軽に問い合わせ頂けると幸いです。

↓↓↓↓