こんにちは、マナボックスの菅野です。

あなたがベトナムでビジネスをしていており、日本の親会社との売り買いがあって、「相殺」できるのか?と思っているのであれば、今回の記事はあなたのお役にたてます。

ベトナムに会社がある。日本の親会社と取引がある。売掛金と買掛金を相殺できないか?疑問がある。その他の論点、例えば税務上のリスクなども気になる。日本ではできるけど、ベトナムではリスクありそうかなと不安。

それでは、詳しく解説していきますね。

この記事のもくじ

【結論】:売掛金と買掛金は相殺できる

結論は、相殺できます。

相殺して後の残高の金額を入金または送金できます。この辺りの細かい手続については、銀行に確認することをおすすめします。

ベトナムでよくある事例、具体例で「相殺」について学びましょう!

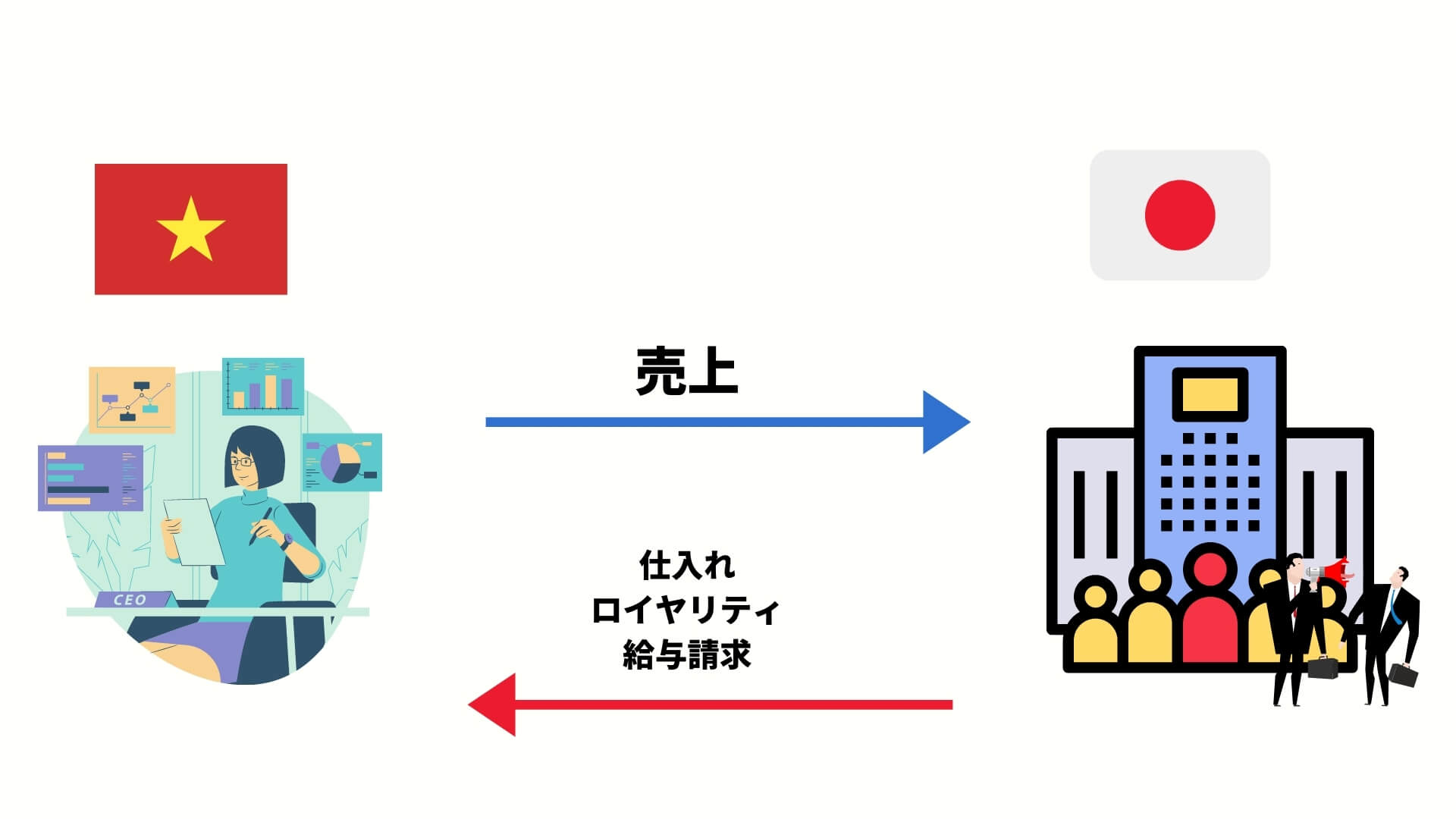

相殺する条件としては、売上と仕入がどちらもある必要があります。深く理解するために、あなたがベトナム子会社の社長であるとイメージしてください。

■ベトナムから本社への売上

EPEなどであればベトナムから本社への売上が生じることが一般的です

■本社からベトナムへの売上(請求)

- 駐在員の給与の請求

- ロイヤリティ

- 原材料の支給

このような事例が多いでしょう。図解もしておきますね。

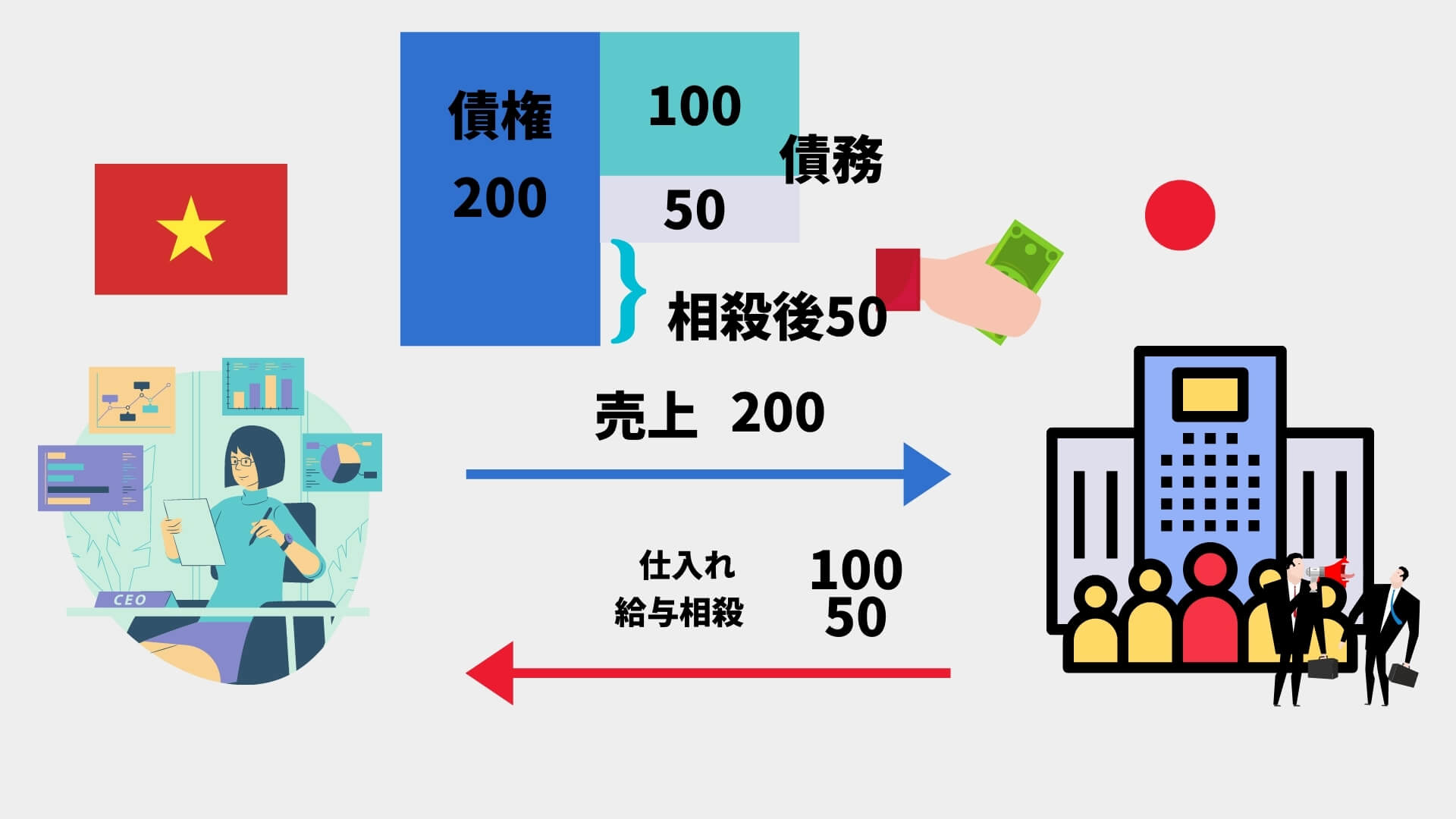

ここで、会計的な視点でも確認していきましょう。具体的な事例で考えてみます。ベトナム側の視点です。

ベトナム会社名:MNV

日本の親会社:MNB

1:MNVは、MNBから原材料を100を仕入れた。

2:MNVは、MNBへ製品を200出荷し、売上を計上した。

3:MNBは、MNVへ駐在員の給与を50請求した。

1:MNVは、MNBから原材料を100を仕入れた。

| 借方 | 金額 | 貸方 | 金額 |

仕入 | 100 | 買掛金 | 100 |

以下の記事も参考にされてください。

>>【徹底解説】BS(貸借対照表)とPL(損益計算書)はこれで動く!会計仕訳を2つのグループと10つのパターンと図解でおさえればスッキリ!

2:MNVは、MNBへ製品を200出荷し、売上を計上した。

| 借方 | 金額 | 貸方 | 金額 |

売掛金 | 200 | 売上 | 200 |

3:MNBは、MNVへ駐在員の給与を50請求した。

| 借方 | 金額 | 貸方 | 金額 |

給与 | 50 | 未払金 | 50 |

この場合、相殺した金額はいくらになり、誰が支払うことになるでしょうか?

- ベトナムがもらえる金額 200

- ベトナムが支払う金額 150

なので、相殺した後は、50の金額をベトナム側が入金されることになります。

ベトナムで相殺した場合、どんなリスクがあるの?なにを準備しないといけないのか?

ベトナムでは、サプライズが結構あります。その中でも税務リスクには留意しないといけません。

では、相殺した場合、どのようなリスクが生じるでしょうか?また、その場合の対応についてもお伝えします。

ベトナム税務上のリスクとそれに対する対応

法人税上の損金算入のリスク

FCT(外国契約者税)が発生してしまうリスク

この2つに整理できます。

では、このリスクに対してどのように対応すればいいでしょう?

結論は、必要な文書を準備すること。これです。

- 当事者間の合意書(売買契約書、売買契約書ともに)にネットオフ方式(相殺)を利用する旨を記載しておく必要があり。

- 買掛金と未収入金の詳細が記載されたネットオフの議事録。

- 銀行送金等の非現金決済方法による支払証憑

ベトナムにおける相殺についての2つの根拠条文は?

根拠についても解説しますね。以下の2つになると思います。

- No. 96/2015 / TT-BTC

- No. 219/2013/TT-BTC

No. 219/2013/TT-BTC

Article 15. Compulsory documents for input VAT deduction

4.Other cases in which non-cash payments are used for deducting input VAT:

a) If goods and services are purchased by offsetting their value against the value of sold goods and services, or by lending goods under contracts, a certification of this kind of transaction and data comparison record made by both parties is compulsory. If the payment is offset against third party’s debt, a debt offsetting record made by all three parties is compulsory.

No. 96/2015 / TT-BTC

Article 4. Article 6 of Circular No. 78/2014 / TT-BTC (amended in Clause 2 Article 6 of Circular No. 119/2014 / TT-BTC and Article 1 of Circular No. 151/2014 / TT-BTC) is revised as follows:

“Article 6. Deductible and non-deductible account when calculating taxable income

1. Except for the non-deductible account prescribed in Clause 2 of this Article, every expense is deductible if all of these following conditions are satisfied:

a) The actual expense expense is related to the enterprise’s business operation.

b) There are sufficient and valid invoices and proof for the expense under the regulations of the law.

c) There is proof of non-cash payment for each invoice for purchase of goods / services of VND 20 million or over (including VAT).

The proof of non-cash payment must comply with regulations of law on VAT.

In case of a purchase of goods and services that are worth VND 20 million or over according to the invoice which is yet to be paid for by the enterprise when the expense is accounted for, such expense will be deductible when calculating taxable income. If the enterprise does not have proof of non-cash payment, the enterprise must remove the value of goods / services without proof of non-cash payment from account in the tax period in which cash payment is made (even when the tax authority and other authorities have issued a decision on tax inspection of the tax period in which such expense is issued).

⭐️本日のまとめ⭐️

- ベトナムの子会社が日本の親会社と売掛、買掛がある場合には相殺可能。

- その場合は必要な文書を準備する。

いかがでしたでしょうか?

あなたのビジネスがベトナムで成功することを祈っていますね。それでは、また!