本日はオフィシャルレターの解説です。2024年6月10日に提出されました。こちらついて解説します。

この文書には、ベトナム財務省税関総局が商工省および計画投資省に対して、ベトナムに物理的な存在がない外国商人の特定方法についてのガイダンスを求めている内容が記載されています。具体的には以下のような内容が含まれています。以下が実際のオフィシャルレターです。

この記事のもくじ

法的背景と定義の不明確さ

ベトナムの外国貿易管理法および商法に基づき、ベトナムに物理的な存在がない外国商人の定義が規定されていますが、その具体的な適用や手続きに関する詳細が不明確であることが指摘されています。

手続き上の問題:

外国商人がベトナムに物理的な存在を持たない場合に、輸出入手続きがどのように扱われるべきかについて、現在の法令では具体的な指針が不足しているため、現場の税関当局が実際の手続きで困難を感じていることが述べられています。

とにかくOn the Spot Export and Import が不明確だからなんとかして!

要するに「On the spot Export and Import(みなし輸出入通関制度政令第08/2015/ND-CP号の第35第1項」の取引についての可否が不明ですよってことです。

今回のお話しをお伝えするためには前提の知識が必要になります。具体的には、ベトナムにおけるOn the spot Export and Import(みなし輸出入通関制度政令第08/2015/ND-CP号の第35第1項の内容をきちんと整理する必要があります。

以下のリンクで詳細に解説しているのでそちらを参照くださいませ。

>>ベトナムにおけるOn the spot Export and Import(みなし輸出入通関制度)の3つのパターンを図解で解説!

これまでもいろんな議論がありました。以下で解説しています!

>>みなし輸出入取引(On the spot import and export取引)の廃止に関するOLの3987/TCHQ-GSQLと4146/TCHQ-GSQLの解説

税関総局からガイダンスの要請:

税関総局(財務省)は商工省と計画投資省に対して、外国商人の特定および関連手続きについての明確なガイダンスを提供するよう要請しています。具体的には、必要な書類や手続きの形式、確認・検証の手順を明確にすることを求めています。

返答の依頼について

税関総局は、貴省に対して2024年6月20日までに書面でのフィードバックを求めており、迅速な対応をお願いしています。

この文書は、ベトナムでの外国商人(日系企業など)に関する規制とその適用に関する問題を解決するためのものであり、関連省庁間の協力を通じて明確な手続きを確立することを目的としています。

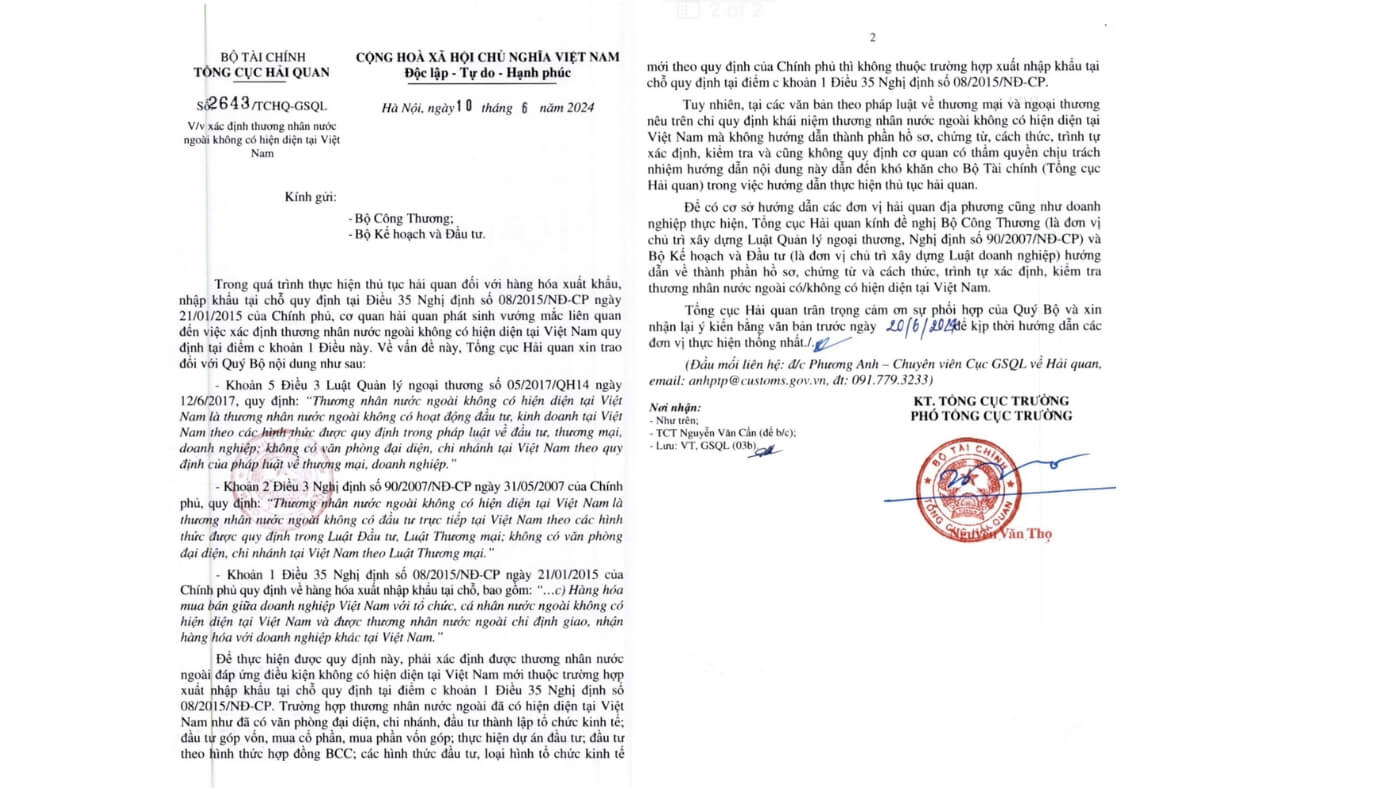

2643/TCHQ-GSQの内容

2643/TCHQ-GSQの英語バージョン

こちら英語バージョンです。